A question for the Coalition for Rainforest Nations: “Why beholdest thou the mote that is in thy brother’s eye, but considerest not the beam that is in thine own eye?”

Yesterday, REDD-Monitor looked at a White Paper put out by the International Emissions Trading Association (IETA) criticising the Coalition for Rainforest Nations’ platform REDD.plus, for claiming that its REDD+ Results Units™ are carbon credits.

Today’s post looks at the Coalition for Rainforest Nations’ response.

On 25 April 2023, CfRN put out a press release under the headline, “IETA publishes false claims about REDD+ sovereign carbon, as voluntary carbon market stagnates in Q1”.

Here’s the first paragraph:

As the voluntary carbon market stagnates and the arrival of REDD+ sovereign carbon looms, the International Emissions Trading Association (IETA) has published a white paper that tries to discredit the use of REDD+ sovereign carbon credits verified under the Paris Agreement for corporate climate claims.

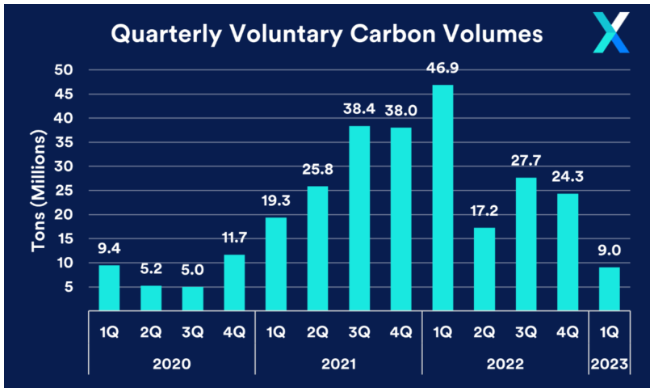

CfRN refers to a report by carbon exchange Xpansiv for the first quarter of 2023 and notes that 9 million tons of carbon were trading in the first quarter of 2023 compare to 46.9 million tons in the first quarter of 2022. CfRN doesn’t mention that the biggest drop, of almost 30 million tons, came between the first and second quarters of 2022:

CfRN describes the first quarter as “disastrous” for voluntary carbon markets, “with forestry project scandals hitting the headlines and VERRA scrambling to introduce new carbon avoidance methodology in response”.

(Verra maintains that its new REDD methodology was started well before The Guardian, Die Zeit, and SourceMaterial exposed serious flaws in Verra’s system, with 94% of its credits having “no benefit to the climate”. Verra states that, “An update to our approach to REDD has been subject to consultation for many years”.)

In the press release, Kevin Conrad, Executive Director of CfRN, states that,

“VCM is struggling, and desperation is now setting in for those holding VCM credits. It comes as no surprise that some of those holding VCM credits within IETA’s membership are coming out with feeble attacks on UNFCCC REDD+ and the sovereign rights of our countries to sell Paris Agreement compliant carbon reductions.”

CfRN argues that “Sovereign REDD+ carbon credits” are authorised under Article 5.2 of the Paris Agreement, and “can be used as carbon offsets by non-governmental entities”.

CfRN summarises two legal opinions which it states were written by two leading law firms working independently:

There are no legal reasons, under the UN Treaties, that REDD+ units in the form of REDD+ Results Units (RRUs) cannot be issued, held, or retired as carbon credits, just like other units generated under UNFCCC mechanisms, such as Certified Emissions Reductions (CER)s and Emission Reduction Units (ERUs).

UNFCCC REDD+ Results, authorized under Article 5.2, can be converted into either a REDD+ Results Unit (RRU) or an Internationally Transferrable Mitigation Outcome (ITMO) type of RRU, and be later used as a carbon offset by non-governmental entities.

RRUs are carbon credits

“REDD+ Results Units are carbon credits,” CfRN states. As such, according to CfRN, RRUs “can be traded within global carbon markets”.

Federica Bietta, Managing Director of CfRN, says,

“Looking ahead, RRUs will be submitted under Article 6.2 beginning this year. Nothing prohibits a Host Party to authorize RRUs as ITMOs under Article 6.2 of the Paris Agreement. There is no restriction under UNFCCC decisions limiting transfer of RRUs to private entities in addition to a country. Claims otherwise are misleading and incorrect.”

IETA argues that RRUs were assessed, but could not be verified because the Warsaw Framework does not set out a standard or method against which it could be verified.

CfRN refers to a UN graphic to argue that RRUs are “indeed verified or assessed under the UNFCCC’s REDD+ Measuring, Reporting and Verification process”:

CfRN claims that UNFCCC REDD+ Results are “the most robust method for crediting the actions taken to conserve the world’s forests”.

CfRN’s press release ends with a statement from Emilio Sempris, former Environment Minister of Panama, who is now part of CfRN’s team:

“The UNFCCC REDD+ framework is more suitable to offsetting claims than what is currently being used by many corporate buyers. These carbon credits are better than anything coming out of the voluntary market. They’re national in scale, so there’s no leakage; the permanence issue is picked up because you have to report every five years; and the reference level is based on hard factual evidence of what your emissions were in the past. They are authorized and issued by the relevant sovereign. None of these principles are in the voluntary carbon market, none.”

Enter CfRN’s “editor-at-large”, Ken Silverstein

Ken Silverstein, a business journalist, wrote two articles for Forbes about IETA’s White Paper. The first, dated 13 March 2023, came after Silverstein received a leaked “rough draft” of the paper titled, “The Evolving Voluntary Carbon Market”.

The second, dated 26 April 2023, is based largely on CfRN’s press release. That shouldn’t come as too much of a surprise since Silverstein’s bioblurb (at the end of the article, visible after clicking “Read more”) reveals that he is “editor-at-large” for CfRN.

I asked Silverstein whether he thought his disclosure note shouldn’t be more prominently displayed. He sent me links to two articles on Forbes that include this statement in the body of the text:

This writer is the editor at large for the Coalition for Rainforest Nations, which represents 53 countries that issue sovereign credits that bypass the voluntary carbon market.

I’d respectfully suggest he should always include that statement in any article he writes about REDD and carbon trading. Particularly when the article is largely based on a press release from the Coalition for Rainforest Nations.

In both articles, Silverstein writes that 200 million tons of carbon credits were traded on the voluntary markets in 2021. “That’s a fraction of the 500 billion tons needed by 2050,” he writes. He doesn’t explain where that figure comes from.

In 2022, global CO₂ emissions reached 40.5 billion tonnes. I might be missing something, but I can’t see the point (even for proponents of carbon offsetting) of the number of offsets increasing to more than 12 times the current global annual emissions rate.

In his 26 April 2023 article, Silverstein writes that IETA’s argument that RRUs cannot be traded on international carbon markets is “an argument tantamount to the taxi authorities telling Uber drivers they can deliver food but can’t carry passengers”.

He accuses IETA of giving “terrible legal advice” when it states that marketing RRUs as carbon credits could “potentially mislead many corporates and expose them to reputational risks . . . ”

Silverstein writes that,

Two unpublished legal analyses — one by an international law firm and the other a global consultancy — conclude sovereign credits are independently evaluated, easily tracked, and transferrable. Those credits are based on historical progress — not future promises, allowing traders to exchange them. Both countries and corporations can purchase them.

It’s interesting that CfRN’s press release states that these analyses were written by two law firms, whereas Silverstein states that one was written by a global consulting firm.

Silverstein writes that CfRN’s sovereign credits are “a threat to the voluntary market” which explains why IETA is “trying to muddy the waters to dissuade companies from buying those credits approved by the Paris Agreement”.

Both of Silverstein’s articles have since been removed from the Forbes website, but archived copies are still available on the Internet Archive.

I asked Silverstein what happened. “IETA complained,” he replied. “My thought was IETA should have a chance to respond by way of op-ed . . . ” but Forbes disagreed.

What’s missing from this discussion

Kevin Conrad argues that the carbon credits that Guyana recently issued are “emissions reductions that never occurred”. He’s probably right. To make matters worse, the carbon credits were bought by Hess Corporation, one of the companies that is extracting oil from the Stabroek block off the coast of Guyana.

But as Simon Counsell, adviser to Survival International, points out in a comment following REDD-Monitor’s post about Conrad’s critique,

“What Conrad also appears not to mention is that the first big issuance of credits under his beloved UNFCCC REDD+ scheme - the 90 million issued to Gabon recently, said to be ‘coming soon’ to Conrad’s trading platform - is that they are purely the result of exactly the same kind of carbon accounting fiddles as the ART-TREES credits from Guyana.

“The carbon market increasingly resembles a bunch of crooks trying to undercut and discredit each other’s ‘fell-off-the-back-of-a-lorry’ goods.”

In June 2022, Gabon’s Forestry Minister, Lee White announced that the country would be making the world’s largest ever issue of carbon credits. Bloomberg noted that the issue of these 90 million carbon credits, if done all at once, could “flood” the market.

So far, Gabon hasn’t sold its 90 million “sovereign credits”. In February 2023, White acknowledged a “lack of interest from buyers”.

Bloomberg describes the problem with Gabon’s “sovereign credits” very succinctly:

The problem, from the carbon market perspective, is that Gabon’s forests have been absorbing carbon for centuries, long before anyone set a net zero goal or issued a carbon credit. That means the climate-cooling benefits they provide are already baked into the global goals for lowering emissions. Carbon credits, though, are designed to encourage additional carbon capture or emissions reductions — in part because companies buy them to offset their own emissions.

Even carbon market proponents are dubious about Gabon’s sovereign credits. Donna Lee is a former US climate negotiator and co-founder of the carbon credit ratings agency Calyx Global. She told Bloomberg that we just don’t have the carbon budget for these carbon credits:

“If each carbon credit is used to compensate for putting a ton of fossil fuel emissions into the atmosphere, then it becomes a trade-off. I don’t know that our carbon budget right now can manage that unless we are confident the transactions result in less, not more, greenhouse gases in the atmosphere.”

Which is pretty much what’s wrong with all carbon offsets.

The reality is that IETA and CfRN are apparently unable, or unwilling, to look at the flaws of the offsets that they are promoting.

Any offset, whether “voluntary” or “sovereign”, exists to allow Big Polluters to continue polluting. While protecting rainforests from destruction is clearly important, if the mechanism for doing so allows continued burning of fossil fuels then it’s a Faustian bargain.

Under both IETA’s voluntary credits and CfRN’s REDD+ Results Units, the deal with the devil is that offsets are sold to Big Polluters - the very companies driving the climate crisis. In exchange for a scheme intended to preserve the world’s rainforests, Big Polluters will rake in eye-watering profits for a few more decades until the planet goes up in smoke.

Finally, someone gets it right - the Bloomberg statement above that "the climate-cooling benefits they provide are already baked into the global goals for lowering emissions." The entire planet has always been involved with solving the carbon cycle problems, that's how the fossil fuels got stored away (not very safely, it appears). Even if a country with a tropical rain forest could demonstrate reduced damage to the forest (end logging, etc.) that act still can’t be sold as an emissions mitigation, since it only serves to bring that forest back up to full operation.

Then Donna Lee mentions that “we just don’t have a carbon budget for these credits,” and for certain, none of these “offsets” has ever resulted in a lowering of the CO2 level, see the Keeling Curve charts. As she says, it becomes a trade-off, an imaginary right to continue to burn fossil fuels.