Risk – the fatal flaw in forest carbon trading?

One of the key issues related to REDD is that of risk. All trade carries an element of risk, but there is general agreement that the risks associated with forest carbon trading might be substantial, and possibly unresolvable, at least in the short term.

Some risks are well known – not the least that forests that are supported by carbon market financing might catch fire, blow down or suffer other catastrophic loss. However, some of the greatest risks relate to the ability (or inability) of tropical country governments to effectively manage large new flows of carbon financing, and to provide the needed stability, governance and ‘enabling environment’ for complex carbon trading regimes to work over necessarily long periods of time.

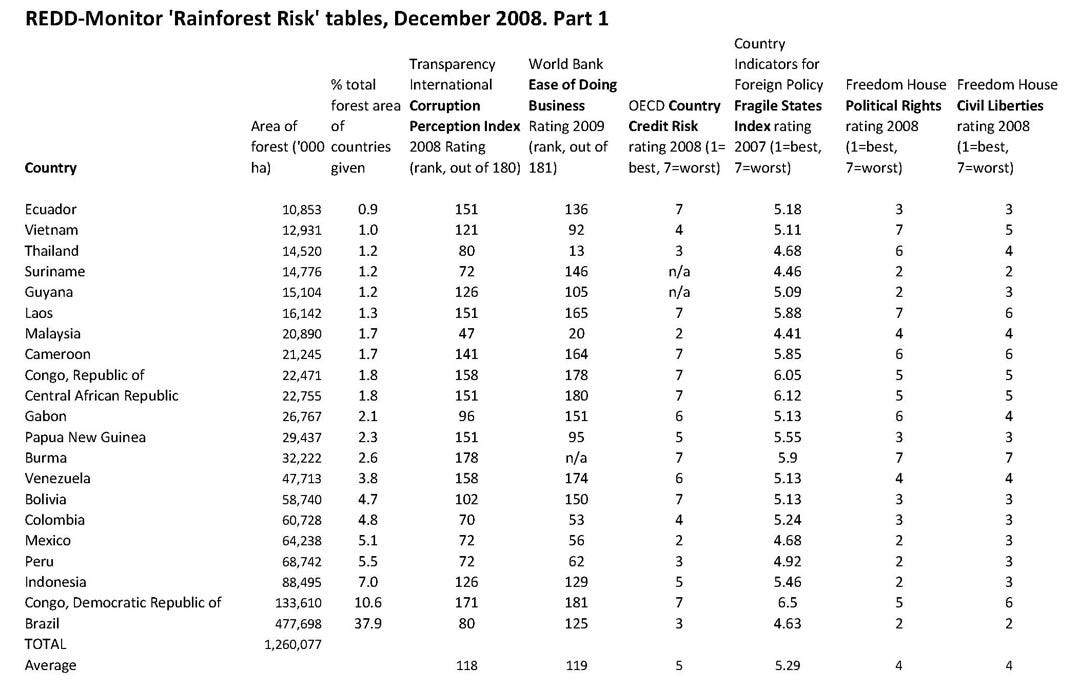

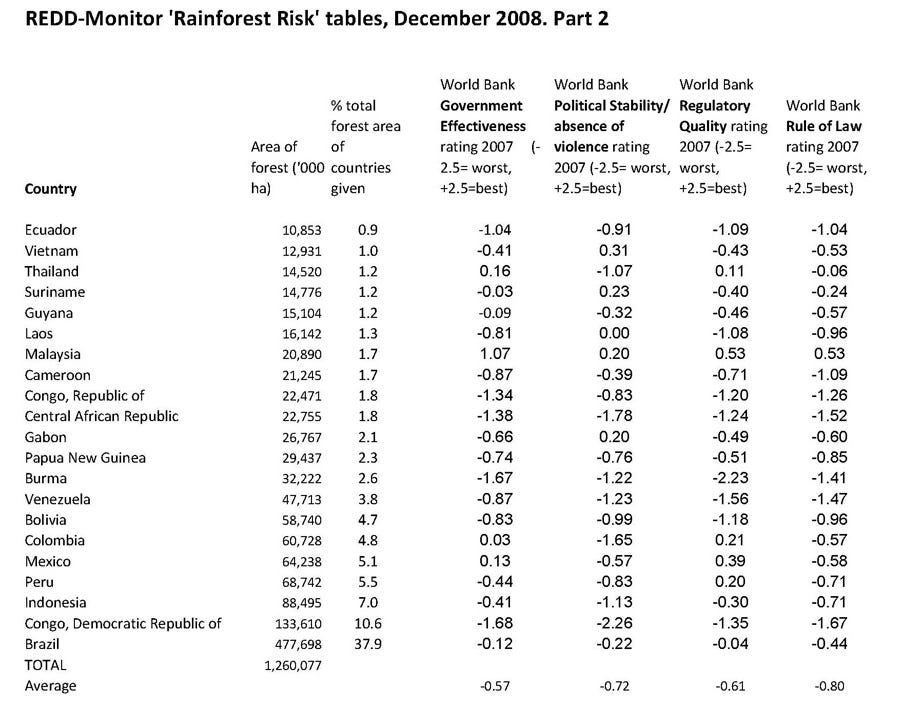

REDD-Monitor has now compiled the ratings and rankings from 10 well-known indices of broad governance performance for the 21 countries with the largest areas of rainforest, which between them contain well over 95% of all tropical rainforests. We show the resulting ‘rainforest risk register’ in full below.

The indices used include Transparency International’s corruption perception index, World Bank governance quality ratings, the OECD Country Credit risk rating, Freedom House ratings on political freedom and civil liberties, and others. The ‘register’ paints a consistent picture of poor governance, high levels of corruption, a mostly bad environment for business, instability, and poor civil liberties.

The data show that, for every single one of the 10 ratings systems, tropical rainforest countries score below ‘half marks’, or fall well below the half way point in global rankings. Using a ‘weighted mean’ calculation which takes account of a country’s rating and its area of forest, the average hectare of rainforest would be in a country ranking 106th out of 180 for corruption, and 124th out of 181 for ‘ease of doing business’. On a scale of 1 (best) to 7, its OECD credit risk rating would be 4.3, and it would be in a country with a ‘fragile state’ rating of a very poor 5.1.

We have not been able to locate any consistent analyses of the risks associated with land tenure, forest policy and legislation, or forestry institutions, though these are known to be seriously problematic in almost every major tropical forest country. The Eliasch Review concluded that around $4 billion would have to be spent over 5 years in order to ‘build the capacity’ of tropical governments for them to be able to properly manage a forest carbon trade – but this amount could well be an underestimate. The history of forestry institution and capacity building in tropical countries has shown that it can be a very long process, and there is now a legacy of decades of neglect, lack of training and expertise in the forest sector and related professions.

Even the strongly pro-trading Johannes Eberling of EcoSecurities has pointed out that there are serious challenges of risk in forest carbon trading. He has noted that only one country, Brazil, offers both a large area of deforestation to be avoided and is relatively low risk – though Brazil is opposed to the notion of forest carbon trading anyway. Eberling has also noted that the impact of high levels of risk is likely be lower prices for forest carbon credits compared with other carbon-reducing projects. Forest carbon in the voluntary markets is already heavily discounted, and selling at only around $2-$3 per ton, compared with credits in the European Emissions Trading Scheme, which are currently trading at around 17 euros per ton.

This may ultimately make little difference to carbon trading companies such as EcoSecurities, who will make a margin whatever the price of the credits, but it might mean that the expectations of some countries of huge financial flows from selling REDD credits are massively over-inflated. The riskier the credits, the higher the proportion of financial flows that are likely to be captured by the traders and ‘carbon middlemen’ in rich countries.

Another likely impact of perceived high levels of risk is that insurers, who would be relied on to underwrite forest carbon trade deals, would probably only be willing to insure REDD schemes over short periods of time – possibly too short to actually be able to detect any measurable ‘avoidance of deforestation’. This problem is likely to become worse because of the impacts of climate change itself, which is expected to cause significant warming and possibly drying of many areas of tropical forest, leading to higher incidences of fire and disease. A spokesman for leading forest insurance group, ForestRe, has said that “Unfortunately, despite what everybody wants, we won’t be getting into 50-year contracts. It will be five rolling years… perhaps rising to 10”.

One solution being proposed for this is that up to half of REDD forest credits could be held in ‘buffer funds’ though this again might mean that much less money from the carbon market would actually become available for disbursement to forest-saving initiatives.

All in all, the risks of ‘doing business’ in forest carbon trading may prove to be prohibitively high, and the returns so much lower, that in the foreseeable future it will only be public funding that can be mobilised on any scale – and this will anyway be necessary over long periods of time in order to reduce the many areas of risk.